Customer Service in Banking: Importance, Strategies & Examples

- March 2, 2026

- 16 mins read

- Listen

In the banking industry, trust and reliability are paramount. Exceptional customer service in banking is not just a support function but a key differentiator. Whether it’s resolving issues, guiding customers through complex financial processes, or simply offering a friendly voice during a stressful situation. The quality of customer service can greatly influence a client’s perception of a bank.

Banking customers want their financial institutions to provide more than just basic service – they want insights, guidance, and relevant recommendations.

A study by Accenture shows that 48% of bank customers preferential treatment and rewards in exchange for their loyalty to your bank.

In this article, let’s explore the importance of customer service in banking, challenges, strategies, examples, and more.

What is Customer Service in Banking?

Customer service in banking is the service a bank provides to both current and potential customers. It includes helping with creating accounts, checking transactions, evaluating loans, and other banking services.

In the banking sector, customer service ensures interactions are fast, consistent, and personalized through calls, live chat, emails, or self-help resources like FAQs or a help center. Thus helping customers resolve issues faster, understand products quicker, and make users feel confident in the bank’s services.

Top 5 Types of Banking Customers You Should Know

Knowing the different types of banking customers helps banks and credit unions understand what people need.

Here are 5 types of banking customers:

1. Conventional Consumers

Conventional consumers value personal relationships and trust in familiar financial institutions. They often visit branches in person and rely on friendly, knowledgeable staff for guidance.

Many focus on saving for retirement and keeping their finances secure. They use online banking occasionally, but only if it is simple and easy to use.

2. Straightforward Savers

Straightforward savers prefer simple, practical banking. They manage basic deposits, withdrawals, and transfers, and like keeping all accounts in one place. Saving money and low fees are very important to them. They do not enjoy complicated banking products or unnecessary changes.

3. Mobile Minimalists

Mobile minimalists handle most banking tasks on their phones. Convenience and speed matter most. They use apps for deposits, transfers, payments, and account checks, and rarely visit branches. They see banking as a tool for managing money rather than building a relationship.

4. Innovative Investors

Innovative investors enjoy trying new tools and technology. They have extra income and like using apps or digital platforms to manage finances. Branch visits are not important to them, and they look for ways to make their money work efficiently through investments or digital advice.

5. Personalized Planners

Personalized planners prefer a combination of digital and in-person options. They carefully plan savings, investments, and loans, and want guidance along the way. They often compare options and appreciate clear explanations.

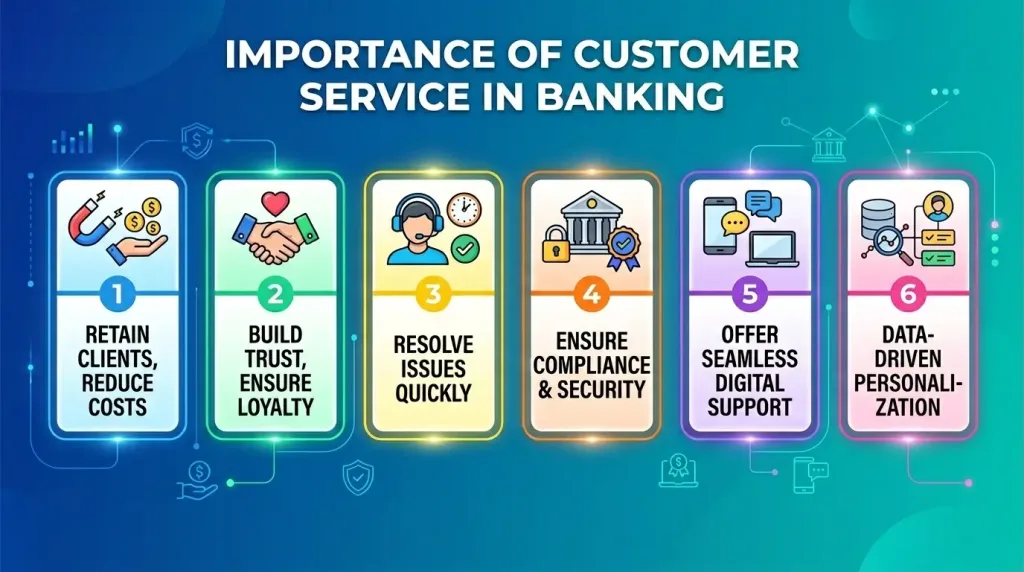

Importance of Customer Service in Banking

For a bank, customer service can be the key differentiator for whether a client stays with you or switches to another institution. With so much competition, customer service in banks has become that much important

Here are six key reasons why customer service is a necessity to retain and attract customers for banks.

1. Retention over Acquisition

Financial Institutions, such as banks, have some of the highest customer acquisition costs (CAC) in the world, making it difficult to attract new customers. Thus, banks have to focus on retaining customers just as much as trying to attract new clients.

By focusing serving current clients, banks can easily foster relationships just by offering exceptional customer service. It doesn’t cost a lot, but the result it brings is tremendous. This keeps churn rates low, business booming, and opening up new pathways for customer acquisition via recommendations, word-of-mouth, etc.

2. Building Trust and Emotional Loyalty

Money is deeply tied to a person’s sense of security, so providing empathetic service is essential for establishing a bank as a reliable partner. When a bank handles a mortgage, a loan, financial transaction mishaps or a college fund with high-touch care, it fulfills an emotional need for stability that automated systems cannot match.

This creates a powerful advocacy effect, transforming standard account holders into loyal brand ambassadors who provide the bank with invaluable word-of-mouth referrals.

3. Rapid Crisis Resolution and Reputation Management

In the complex world of finance, technical glitches or fraudulent charges are high-stakes emergencies for the customer, making rapid support an operational necessity. Maintaining accessible and expert support channels ensures these stressful moments are neutralized before they escalate.

Effectively resolving these issues protects the bank’s public reputation and prevents a single technical error from turning into a legal complaint or a viral social media crisis.

4. Regulatory Compliance and Risk Mitigation

Banking is a heavily scrutinized industry where providing inaccurate information can lead to massive fines or the loss of an operating license. High-quality customer service ensures that every interaction is accurate, ethical, and follows strict data privacy laws.

This adherence to standards acts as a safety net for the institution, mitigating legal risks and ensuring the bank maintains the high level of integrity required by both regulators and the public.

5. Seamless Digital Transformation

Modern consumers now expect 24/7 access to their funds and instant support across all devices, from mobile apps to AI chatbots. It is vital for banks to merge their physical and digital support into one seamless experience to remain relevant in a tech-heavy market.

Successfully mastering this journey allows a bank to capture a younger, tech-savvy demographic and differentiates the institution from traditional banks that are slower to adapt.

6. Data-Driven Personalization and Revenue Growth

Banks sit on a goldmine of transaction data that allows them to understand a customer’s specific life stage and financial goals. Using customer service as a platform to offer proactive financial advice, rather than just waiting for a customer to call with a problem, shifts the bank’s role to that of a financial advocate.

This proactive approach significantly increases cross-selling opportunities, as customers are far more likely to purchase insurance or investment products from a bank they feel truly understands their needs.

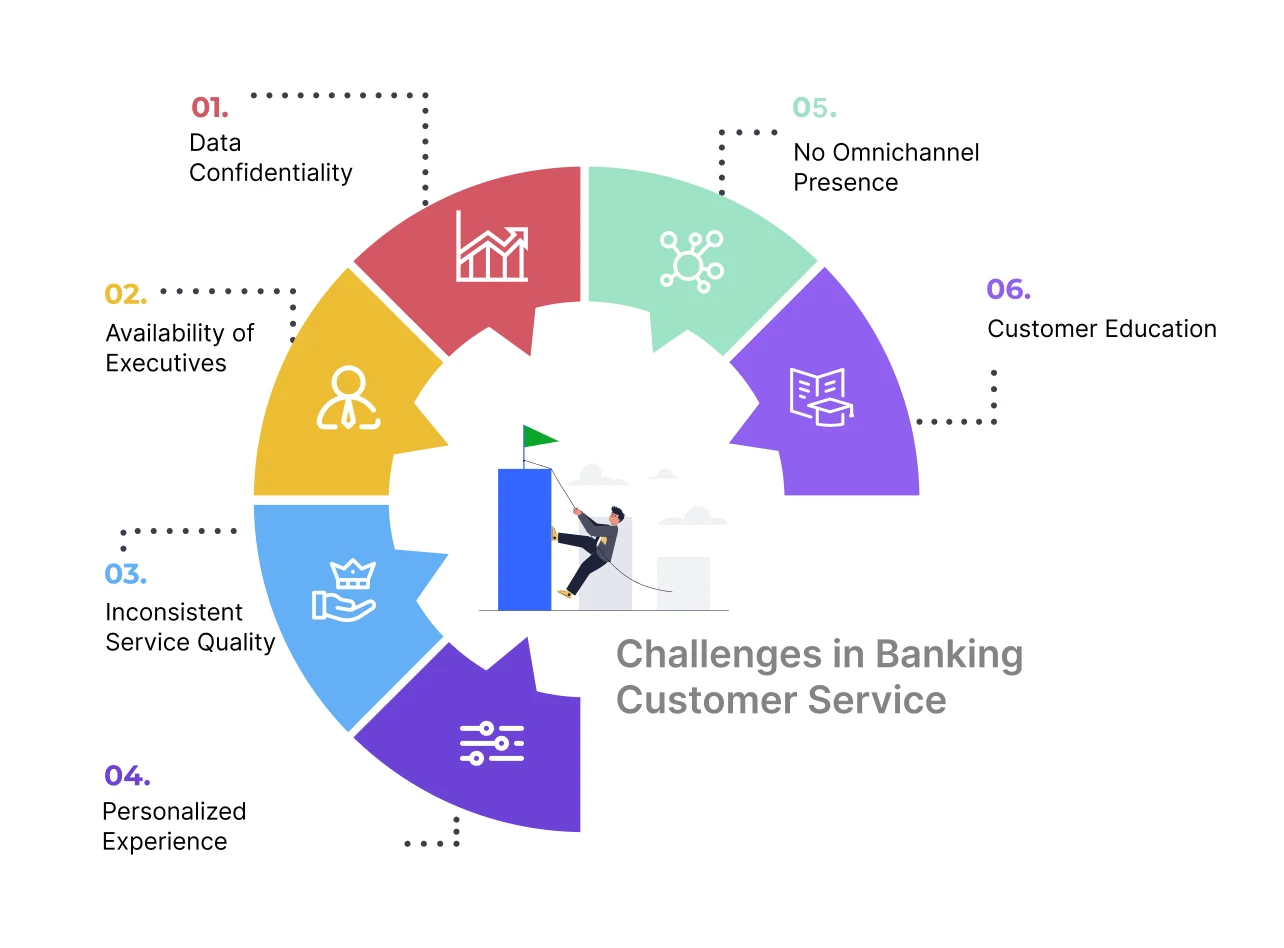

What Are the Common Challenges in Banking Customer Service?

Offering the desired customer service to a customer is a big challenge in a bank. Let’s find the most common challenges bank faces that impact the overall customer experience:

- Data Confidentiality: It is a vital aspect for banks. Privacy and security of customer data are paramount for banks. They must secure sensitive information from breaches and unauthorized access while maintaining customer trust.

- Availability of Executives: In a banking setting, it’s very common that customers often need more access to banking executives. In particular, during peak hours. There is no doubt that long wait times and inadequate availability of staff are responsible for customer frustration and dissatisfaction.

- Inconsistent Service Quality: Consistency is crucial to maintain a high standard of service. However, variability in service quality across different branches or even among individual representatives can affect customer experiences.

- Personalized Experience: Another challenge in banking customer service is to deliver personalized customer service to each customer. Banks must effectively use customer data to offer personalized solutions and recommendations.

- No Omnichannel Presence: Customers expect automated interaction across various channels, including in-person, online, and mobile. A lack of integrated omnichannel support can lead to fragmented and frustrating experiences. For example, Bank of Scotia and Bank of Kuwait picked REVE Chat omnichannel customer engagement solutions to serve their customer faster.

- Customer Education: In many cases, educating customers is a big challenge. Helping customers understand and use new banking products and services is crucial. Banks need to invest in educating their customers to enhance their banking experience and build long-term relationships.

How to Improve Banking Experience for Customers

Customers feel ignored when they get poor service in banking. Keep in mind that slow response, repeated transfers between staff, or difficulty reaching help can push customers away.

Banks can improve service by focusing on personal attention, speed, accessibility, and technology.

So, they can improve customer service in banking by:

Understanding Customer Needs

Every customer has different goals and habits. Banks should offer services that fit each person. Sending reminders, updates, or suggestions shows that the bank pays attention.

Quick and Accurate Support

Customers expect problems to be solved quickly and correctly. Staff should respond fast and make sure issues are fully resolved. Quick and accurate service helps customers trust the bank.

Options for Self-Service

Self-service tools let customers manage accounts on their own. Online banking, mobile apps, and automated kiosks allow people to complete transactions without waiting for help. These tools should be simple to use. Staff should still be available for customers who prefer talking to someone.

Proactive Communication

Reaching out before issues appear shows the bank cares. Sending reminders about payments, updates, or account changes prevents problems. Proactive communication is an important part of customer service in banking.

Guidance and Support

Helping customers understand banking tools builds confidence. Providing instructions, tutorials, or in-branch help ensures customers can use apps and online banking effectively. Understanding their options helps customers make better decisions.

Support in Multiple Ways

Customers need help in different ways. Offering support by phone, email, chat, video, and in person ensures everyone can get assistance. Consistent service across channels makes it easier for customers to get help.

Feedback and Improvement

Listening to feedback helps banks improve. Observing which services customers use and where they face difficulties allows adjustments. Acting on feedback shows customers that their opinions matter and strengthens customer service in banking.

Using Technology to Help

Technology can make banking customer service faster and easier. Here are some key points on how technology can help banks with customer service:

1. Artificial Intelligence

AI chatbots and virtual assistants provide help at any time. They answer simple questions and allow staff to focus on more complicated requests. This helps customers get support quickly.

2. Data Analysis

Studying customer habits helps banks provide services that match what people need. This improves communication and service.

3. Security Tools

Security measures protect accounts and transactions. Customers feel confident when banks protect data and prevent fraud.

4. Combining Communication Options

Providing support through multiple channels lets customers choose what works for them. Starting a conversation on one channel and continuing on another without repeating information makes it simple and clear.

5. Live Chat and Chatbot Support

Adding live chat and chatbot support helps banks reply quickly and manage more customer questions with ease. A platform like REVE Chat offers both live chat and chatbot services where you get real-time messaging, simple AI tools, and secure communication. This helps banks assist customers faster and reduce wait times across all channels.

Creating a Customer-Focused Culture

A culture that values care improves every interaction. Training staff to listen, explain clearly, and respond patiently ensures customer service in banking is effective. Banks that focus on care keep customers loyal.

Regular Updates and Adjustments

Customer needs change. Banks should review processes, update tools, and train staff regularly. Regular improvements keep customer service in banking effective and relevant

7 Examples of Excellent Customer Service in Banking

Technology is rapidly changing the way we work, communicate, and bank. Those who are steering the ship understand the importance of not only better meeting consumers where they are today but also planning ahead to proactively address new needs in the future.

The following financial service leaders are freeing up members of the team to deliver higher levels of service and tailor offers to make banking more personal.

1. Commercial Bank of Kuwait (Kuwait)

Challenges: Handling a wide range of customer inquiries, from card issues to loan eligibility, while delivering fast, accurate, and personalized responses in a competitive market.

Achievement: The Commercial Bank of Kuwait adopted REVE Chat’s comprehensive customer engagement tools, including Live Chat, forms, canned responses, chat tags, and notes, to address diverse customer needs efficiently.

Agents use this platform to resolve issues like prepaid MasterCard functionality, provide card delivery updates, assess loan and credit card eligibility, and guide customers to the nearest branch or service, ensuring quick and tailored support.

Why it works: REVE Chat’s streamlined features, such as canned responses and chat tags, enable agents to deliver consistent and rapid assistance, while Live Chat facilitates real-time customer engagement.

Tools like forms and notes simplify complex queries, such as loan applications or username recovery, by organizing customer information effectively.

By integrating this versatile platform, the bank has reduced response times, improved issue resolution rates, and built stronger customer trust through accessible and personalized support.

2. Veritas Finance (India)

Challenges: Streamlining loan management processes while ensuring customers have instant, user-friendly access to account services.

Achievement: Veritas Finance integrated REVE Chat’s powerful chatbot, SDK, and API solutions to transform its loan management and customer service operations. With the platform, customers can effortlessly view active and closed loans, request account statements or welcome kits, initiate prepayment or closure processes, update contact details, and access CIBIL reports directly through a seamless chatbot interface.

Why it works: REVE Chat’s intuitive automation empowers customers with self-service capabilities, significantly reducing reliance on manual support while speeding up tasks like document submission and loan closures.

Features like instant statement generation, NOC or MODT requests, and credit bureau assistance provide clarity and convenience, ensuring customers feel in control of their financial journey.

By leveraging the customer engagement platform, Veritas Finance has boosted operational efficiency and elevated customer satisfaction with a personalized, digital-first experience.

3. Navy Federal Credit Union – Delivering effective omnichannel experiences

Virginia-based Navy Federal Credit Union exclusively serves the military, veterans, and their families, a segment to which it promises “once a member, always a member.”

Great customer service is important in delivering on this promise, and the Navy Federal Union realized that.

“As a lender, it’s really important for us to be consistent in the member service experience,” explained Prabha KC, a mortgage loan officer at the company. “If the members are overseas, they can still access their loan information.”

Offering self-service channels was one way the company sought to improve its service delivery, not only facilitating 24/7 support but also freeing up its member service representatives to do more added-value work on behalf of their members.

As a result of the implementation, the number of self-service applications doubled, and the time taken to submit an application decreased by 40%.

4. BOK Financial – Making banking more personal

Investing in personalization empowers banks to deliver the white glove service that customers are looking for. In fact, the majority, 72% of customers, say that personalization is highly important in financial services today.

Oklahoma-based BOK Financial adopted strategies to help it meet consumer demand for an intuitive and personalized banking experience.

By running consumer loans and mortgage applications, the company is delivering a tailored experience and, as a result, has seen completion rates more than triple. Moreover, the majority of volume now comes through digital channels, in stark contrast to the previous 15%.

5. Amarillo National Bank – Adapting and responding to new needs

When banking teams prioritize their customers’ needs and preferences, they can deliver better service, and they can achieve more impactful customer relationships as a result.

During the global pandemic, many lenders, including Texas-based Amarillo National Bank (ANB), searched for ways to continue closing loans remotely. The value of hybrid and electronic closing methods quickly became clear.

“We knew we had to move forward with the hybrid closings so that our customers didn’t have to go into the title companies to close their loans,” Debbie Bigelow, senior vice president, recalled. They will continue to adopt innovations that allow them to succeed in a rapidly changing operating environment.

6. Chase Bank (USA)

Challenges: Chase Bank encountered serious issues in handling a high volume of customer inquiries and complaints.

Achievement: They invested in advanced customer service AI bots to meet consumer demand for intuitive and personalized service. These bots triage and resolve common queries quickly. This allowed human agents to focus on more complex issues.

Why it works: Chase Bank enhanced operational efficiency and significantly reduced wait times just by automating routine interactions. But what result did it bring? Customers appreciated the immediate responses from AI bots for simple queries, while more complicated matters received dedicated attention from human agents. This balance improved overall customer satisfaction.

7. DBS Bank (Singapore)

Challenges: Integrating automated digital banking solutions while maintaining personalized customer interactions.

Achievement: DBS Bank launched a comprehensive mobile banking app with AI-powered chatbots for instant support, meeting consumer demand for convenience and personalization. Proactive notifications keep customers informed about their account activities.

Why it works: Combining digital convenience with personalized service, DBS Bank effectively caters to diverse customer needs. The app’s user-friendly interface and real-time assistance made banking more accessible and efficient, while proactive communication helped build trust and prevent issues from escalating.

End Note

In the end, good customer service in banking builds trust, loyalty, and long-lasting relationships. Banks that listen to customers, give clear guidance, and respond quickly create a better experience for everyone.

Using digital tools like mobile apps, live chat, AI chatbots, and omnichannel platforms makes support faster and easier for customers.

Looking for the best tool to offer the best customer service? REVE Chat helps banks provide real-time support with live chat, chatbots, and video chat, improving response times and personalizing interactions.

A 14-day free trial is available with advanced features, so try it today.

Frequently Asked Questions

You can see your account balance through online banking mobile app, ATM, or by calling our customer service.

You can customer service right away to block the card and stop unauthorized transactions. You can ask for a new card too.

To set up direct deposit, give your employer your bank account number and routing number. You can find this info in your online banking portal or by calling the bank’s customer service.

You can send money to another bank account via online banking mobile app, or by going to a branch. Your options include wire transfers, ACH transfers, and person-to-person payments.

The charges change based on your account type and the services you use. You can find a complete list of fees on our website or by getting in touch with our customer service team.